Beauty, consolidation slows down but the market prepares for a new M&A season

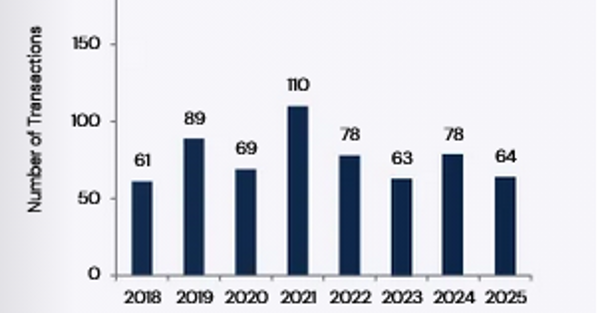

In 2025, M&A's activity in the sector slowed down significantly: the number of deals fell by 17.9% year-on-year

The beauty industry is slowing down on the mergers and acquisitions front, but the market continues to prepare for a new phase of consolidation. Although the break-up of negotiations between Puig and Estée Lauder, which would have led to the creation of a $40 billion global group, came as an icy shower to the sector, which had hoped that the deal would trigger a chain reaction for medium-sized companies as well.

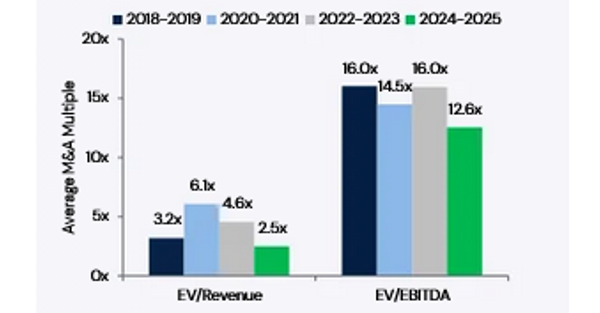

In 2025, M&A activity in the sector experienced a significant slowdown: the number of transactions declined by 17.9% year-on-year, stopping at 64 transactions, in an environment still affected by macroeconomic uncertainty, geopolitical tensions and the redefinition of global trade balances. The data emerged from the Annual Consumer M&A Report by Capstone Partners, a US investment bank focused on the middle market segment.

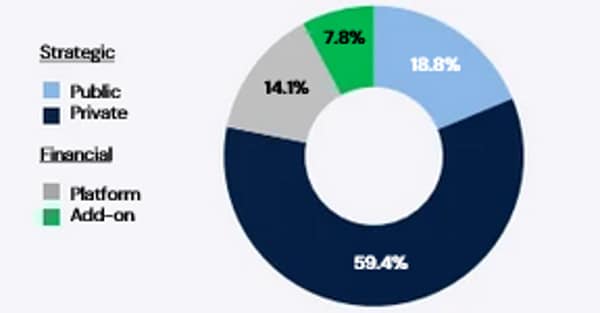

Despite the slowdown, according to Capstone's traders, the structural conditions of the sector remain solid. Supporting expectations of an upturn in operations are the resilience of beauty demand, higher growth than in other consumer verticals, and the continued emergence of independent brands capable of reaching significant size quickly. It is precisely these emerging brands that are becoming increasingly central to the acquisition strategies of large international groups.

"The attractiveness of the beauty sector is particularly evident over the past three years, a period in which much of the consumer discretionary sector has been severely penalised, while beauty has continued to show resilience," comments Ken Wasik, head of investment banking at Capstone Partners, who continues: "Strategic buyers continue to fuel the demand for quality beauty assets, while private equity funds have become much more selective and, at least for the time being, tend to retain their existing holdings in the sector. In this context, it is a favourable time to enter into discussions with strategic buyers,' adds Wasik.

Investor focus

In a scenario characterised by increased volatility and a growing focus on geopolitical and tariff balances, investors have gradually shifted their focus from growth rates alone to economic fundamentals and the quality of profitability. In 2025, the most sought-after assets were those offering vertical integration, exposure to clean beauty and wellness segments and potential for international expansion. Also particularly attractive were brands that allow foreign operators to get closer to the end consumer through a stronger local presence and direct customer relationships. According to analysts, these assets could be key players in competitive sales processes even in 2026, especially in a context where many international companies are seeking to strengthen their control over distribution and the customer experience.