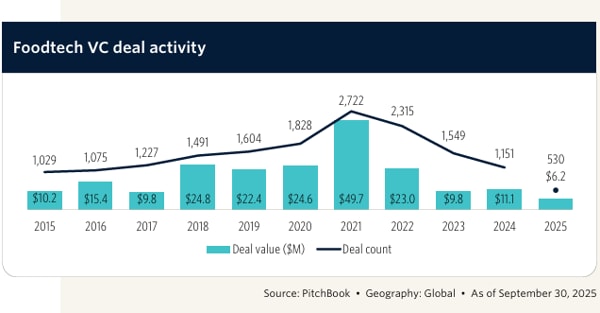

Foodtech, food innovation no longer of interest to venture capitalists

In Q3 2025, 148 deals with a total value of USD 2.8 billion were completed, down 44.6% year-on-year.

Key points

Decline in interest in the foodtech sector by venture capital funds. In Q3 2025, 148 deals with a total value of USD 2.8 billion were completed, down 44.6% year-on-year. The trend during the period was a strong focus on established players, with Wonder Group's $1.1bn mega-round alone accounting for 40.1% of capital raised, while the top 20 deals accounted for 78% of total deal value, although the trend of maxi deals in the sector is declining when looking at the long term, according to data from the PitchBook report on the sector.

Looking at the trend since the beginning of the year, there are 530 deals for only USD 6.2 billion, far from the 2021 peak of 2,722 deals for a total amount of USD 49.7 billion.

There was also a negative trend in divestments: exit activity plummeted to 14 transactions, since many start-ups have not yet reached a sufficient size to be able to go public or do not have attractive profitability levels to attract the attention of industrial groups. This is precisely why funds have had to resort to secondary market transactions or debt instruments.

Dominate the late-stage

The quarter showed a deep structural bifurcation in the market. Thesize of round early-stageincreased 21.2% year-on-year, while median valuations declined 52.4%, falling to $7.5 million on average. Pre-seed/seed valuations fell 12.8% to $7.8 million, while those late-stage valuations rose 28.4% to an average of $29.4 million. This dynamic, according to PitchBook, is set to continue through 2026, requiring founders to be more diluted to raise the same amount of capital and the need to accelerate the achievement of concrete results between rounds.

In Q3 2025, a strong divergence emerged between the different investment stages compared to cumulative trends since the beginning of the year. Although the YTD distribution was balanced between late-stage VC (51.3%), early-stage VC (18.5%), pre-seed/seed (17.7%) and venture growth (12.5%) out of a total of 530 deals, the 148 deals in Q3 concentrated the bulk of capital on late-stage winners. Late-stage VC raised $2.6 billion, or 92.7% of the quarter's capital, on 110 deals, a much higher share than the 51.3% recorded from the beginning of the year to the end of September. Early-stage and seed, on the other hand, raised a total of only $207m (7.3% of the quarter's capital), down sharply from $525m in Q2024.