The friendly statement goes digital, filling it out incorrectly can lead to loss of cover

It will remain possible to report a claim even with a paper form. But companies prefer more certain evidence and the Supreme Court approves

4' min read

Key points

4' min read

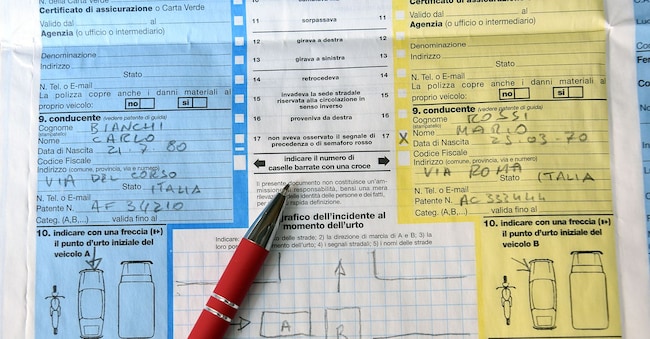

The Cai form (Authorised Accident Declaration, also known as Cid or blue form) becomes digital. It is one of the biggest novelties of theIvass regulation no. 56 of 25 March 2025, a further step forward in the digitalisation of motor liability documents. It was inevitable that the Cai too would have a digital version, as was already the case for the insurance sticker and certificate.

With the Cai every driver involved in an accident (whether right or wrong) fulfils the obligation to report the accident, filling in the fields and giving the company a detailed description of the dynamics and consequences.

The rule remains valid according to which, when the accident involves two vehicles and the Cai is signed by both drivers, it is presumed that the dynamics and consequences are those indicated on the form, unless the companies can prove otherwise. In all other cases (including those occurring abroad or also involving vehicles with foreign number plates), the Cai is in any case a useful trail to collect all the evidence needed to determine liability and settlement.

Article 143 of the Insurance Code (Cap) also gives the Cai an important evidentiary value: if it is signed by both drivers involved, it is presumed, unless the insurance company proves otherwise, that the accident occurred as shown on the form (on the possibility of overcoming this presumption, especially if technical checks reveal incompatibilities, see, among others, ruling 2438/2024 of the Court of Cassation).

Precisely because it is important for evidentiary purposes, the paper Cai (once even compiled on copy paper) - easily altered - has often been the focus of fraudulent conduct. The digital medium should greatly reduce this risk, with an unalterable traceability of what is described.