AI, capital raised in Q1 exceeds entire 2025

Private companies raised a total of EUR 226 billion in the first three months of this year

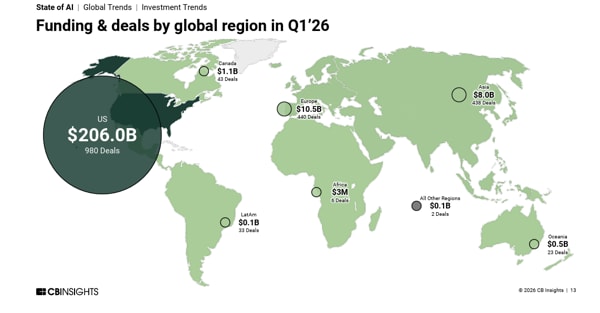

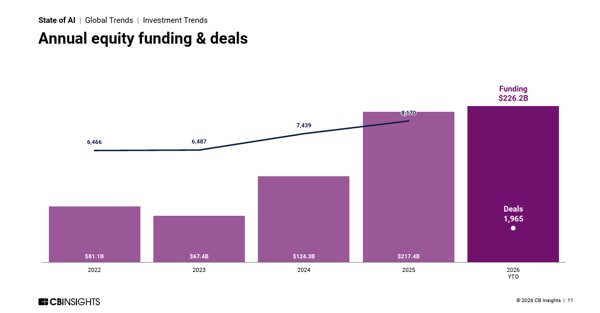

In the first quarter of 2026, the global artificial intelligence market for private (unlisted) companies experienced unprecedented growth, with the total amount raised amounting to $226 billion in 1,965 deals globally. A level that, in just three months, surpasses the entire amount raised during 2025 of $217 billion in 8,170 deals, marking a significant acceleration in capital flows to the sector.

The mega deals

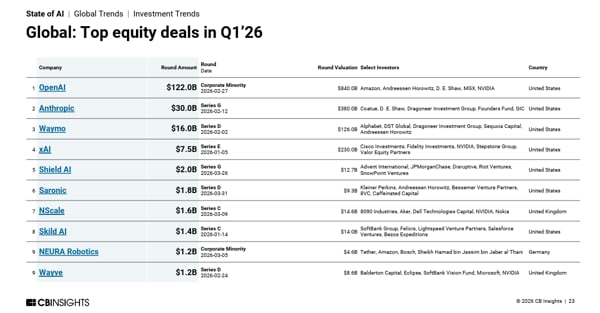

A single transaction was the key driver of the market: the $122 billion round closed in early April by OpenAI for a post-money valuation of$852 billion, which alone accounted for 54% of the quarter's total funding. Net of this round, first-quarter funding would stand at $104 billion, still up 45% quarter-on-quarter, compared to $72 billion in the final quarter of 2025.

The period was dominated by mega-rounds: deals in excess of USD 100m catalysed 94% of capital raised, up from 80% in the previous quarter. This dynamic pushed the average deal size since the start of the year to $159.9m, more than four times the annual average of $38.2m recorded in 2025.

The most active sectors

On the sector front, the dominance of large language models (LLM) persists. In addition to OpenAI, Anthropic (USD 30 billion in a Series G round in February for a total valuation of USD 380 billion) and xAI (closed a USD 20 billion round in January, bringing the valuation to USD 200 billion) also completed multibillion-dollar deals, confirming the centrality of model developers in catalysing investments.

Alongside this strand, the 'physical AI' segment is emerging with increasing significance. In the quarter, 11% of all transactions in the AI segment involved companies active in robotics, defence technologies and autonomous systems, signalling a broadening of industrial and infrastructure applications of artificial intelligence. The quarter also confirmed the pace of global unicorn growth seen in the last 2025 quarters: 21 new companies surpassed the billion valuation mark, bringing the total number to 390 at the end of March.