Valentino ends 2025 with a decline: revenue at 1.12 billion, EBITDA down 41 per cent. Debt rises

The fashion house, which is majority-owned by the Qatari fund Mayhoola (70%) and in which Kering holds a 30% stake, has seen a decline in sales across all regions

2025 proved to be a challenging year for Valentino, which closed its financial year with a sharp decline in revenue and profitability, against a backdrop of a general slowdown in the luxury market and weaker demand in almost all geographical regions. According to the financial statements filed by the Rome-based fashion house, turnover stood at €1.12 billion, down 15% on the previous year, whilst earnings before interest, taxes, depreciation and amortisation (EBITDA) fell by 41% to €174 million. Net debt also rose, climbing to €1.13 billion from the previous €1.08 billion.

In the document, the company explains that exchange rate movements also weighed on the results: “Currency movements had a negative impact of approximately 2 percentage points, mainly attributable to the strengthening of the euro against the US dollar, the Japanese yen and the Chinese renminbi.”

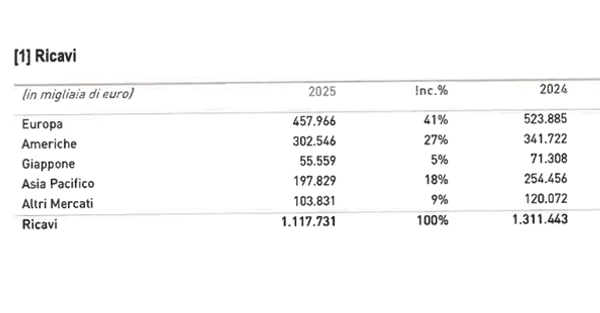

The geography of revenue

“The slowdown affected all geographical areas, with a more pronounced decline in Japan and the Asia-Pacific region,” states the commentary on the financial results, which cites among the causes “a decline in consumer confidence” and the adverse effects of currency fluctuations on tourist numbers.

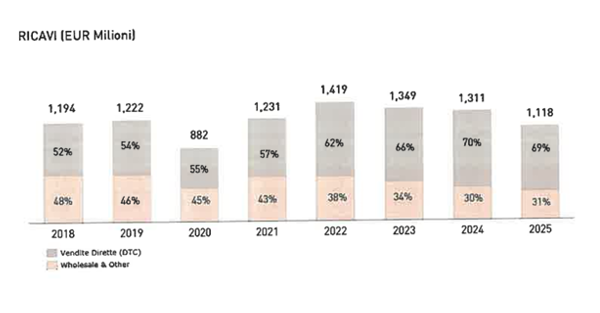

The slowdown was felt most acutely in the direct retail channel. The financial statements reveal that ‘these factors had a predominant impact on direct-to-consumer sales, which were affected by a reduction in footfall at retail outlets and more cautious purchasing behaviour on the part of customers’. The wholesale sector also suffered a setback, with ‘a significant decline in volumes’.

By geographical area, Europe was affected by a slowdown in domestic demand and a return to more normal levels of tourist flows. The company notes that ‘in 2025, revenue in Europe fell compared with the previous financial year, reflecting weaker domestic demand and a normalisation of tourist flows following the strong rebound recorded in previous years’. Another contributing factor was the reduction in orders from commercial partners, with the wholesale channel “having a negative impact on the region’s overall performance (-14% at constant exchange rates)”.