M&A, Goldman Sachs sees a 3.8 trillion market in 2026

Mergers and acquisitions activity will be led by the artificial intelligence sector and divestments by private equity

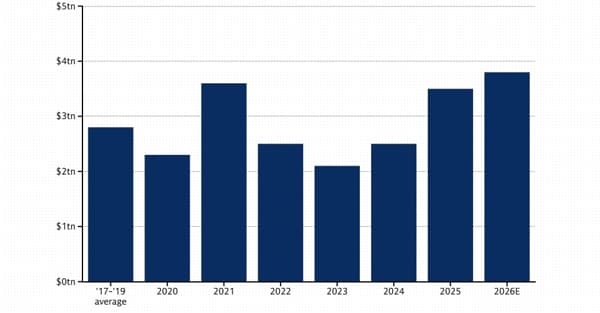

The global M&A market could reach$3.8 trillion by 2026, buoyed by activism in the artificial intelligence sector and accelerating divestments of holdings by private equity funds. The estimate of the total amount is from Goldman Sachs Global Banking & Markets, which identifies further room for expansion in the current cycle in light of the positive trend in the first quarter of the year.

The market, according to Tim Ingrassia, co-head of global M&A at the investment bank, is currently in the fourth year of a cycle that historically spans a six- to seven-year horizon. A phase that still tends to be expansionary despite the macroeconomic environment characterised by high uncertainty. On the other hand, at this stage, extraordinary transactions remain a central tool in the strategies of industrial groups and CEOs, notes Ingrassia, continue to resort to M&A to strengthen the long-term value of companies, also in relation to the industrial transformations induced by artificial intelligence.

The mega deals

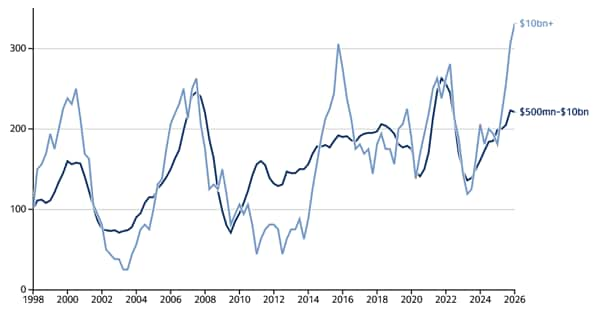

In 2025, deals larger than $10 billion increased 24% from the previous high in 2021, according to Dealogic data. A trend that historically anticipates a broader expansion of the market, thanks to the ability of large players to move more quickly and generate knock-on effects on overall activity.

Goldman Sachs points out that, adjusted for spin-offs, financing rounds of unlisted companies and SPAC transactions, the 'pure M&A volume' may be at its highest level in recent years, with a gradual strengthening of the current cycle.

Two structural factors in particular are underpinning M&A's activity: on the one hand, the search for organic and inorganic growth in a context of accelerated technological transformation; on the other hand, the need for private equity to monetise the holdings in its portfolios (which are now ageing more than the historical average) and return capital to investors. Indeed, buyout fund distributions remain at historically low levels, thus increasing the pressure on divestments as the impact of the failure to return capital to investors is being felt on the fundraising side of new funds.