M&;A, traditional guarantees collapse and risks shift to insurance

The legal and contractual risk of transactions is progressively transferred from the parties to the policies and contracts are increasingly standardised even in the middle market

The M&A market in 2025 is changing profoundly, with insurance playing an increasingly central role. According to the new 2026 Deal Terms Study published by SRS Acquiom, the US middle market is undergoing a structural transformation: the legal and contractual risk of M&A transactions is progressively being transferred from the parties to Representations & Warranties Insurance (RWI) policies, profoundly changing the market for extraordinary transactions for unlisted companies.

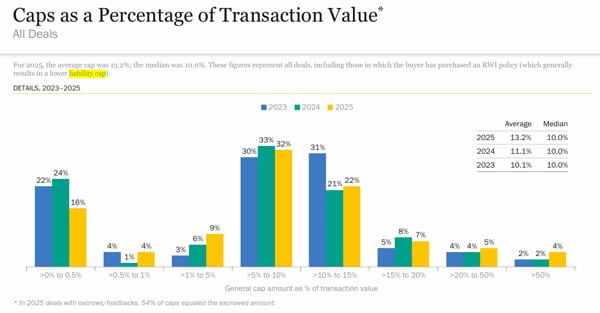

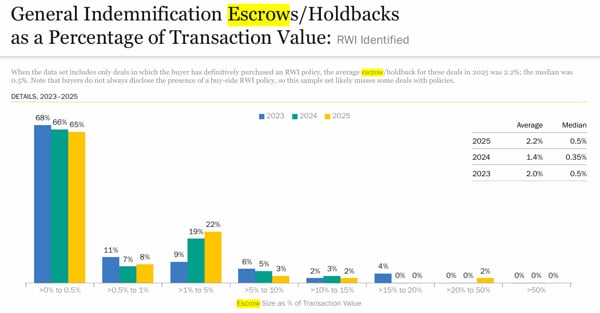

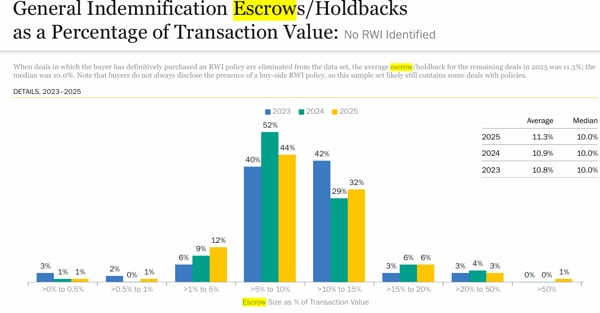

The phenomenon emerges clearly from the data on escrow (the share of the price temporarily retained as post-closing security), liability cap (the upper limit to the damages that the seller can be obliged to indemnify) and persistence of representations and warranties (the period during which the seller's warranties remain valid after closing), which show an increasingly standardised, liquid and seller-friendly market. In particular, the most emblematic figure concerns the escrow post-closing. In 2025 transactions with identified RWI, the median escrow falls to 0.5% of the transaction value, compared to 10% in transactions without insurance coverage.

In practice, buyers retain a smaller and smaller share of the amount paid as security for possible future disputes, relying on insurance companies rather than the seller's assets to cover the risk.

In transactions without insurance, the amount retained was in 2025 in 44% of cases between 5 and 10% and in 32% of cases between 10 and 15%. The percentage of transactions without insurance that had an escrow below 0.5% was negligible (1%). This demonstrates how the risk, in the presence of insurance, is minimised for the seller.

Reduced liability limits

The same dynamic emerges from liability caps (liability cap). In deals with insurance coverage (Rwi), the median seller liability cap stops at 0.5% of the transaction value in 2025, while in deals without Rwi the figure rises to 10%. This is a radical change from the traditional structure of US middle-market M&A deals, historically characterised by long periods of seller liability, consistent escrow and high residual seller exposure after deal closing.