Kering, revenues down 16% and profit halved in the first half of the year

Turnover fell by 16% to 7.587 billion and the group's net attributable profit fell to 474 million from 878 million in 2024

6' min read

6' min read

New quarter down for Kering, with negative performance across all geographies. The French luxury group ended the first half of 2025 with revenues of €7.6 billion, down 16% on a reported basis and 15% on a comparable basis. The performance reflected a particularly difficult market environment, to which the group responded with targeted actions on its cost structure and a strategy of financial strengthening.

Recurring operating profit amounted to EUR 969 million, with an operating margin of 12.8% (down 4.7% year-on-year). Net profit attributable to the group was EUR 474 million, down sharply from EUR 878 million in H1 2024, a decrease of 46%.

"The first half of 2025 represented a period of significant strategic decisions for Kering. On the governance front, I proposed to the board of directors, which was favourably received, that Luca de Meo be entrusted with the role of ceo of Kering, while I will retain the chairmanship of the board. At the creative level, the strengthened teams, led by new artistic directors in three of our major maisons, are working with passion and determination to increase the desirability and enhance the heritage of our brands. At the operational and financial level, in a particularly difficult market environment, we continued to rationalise our distribution network and cost structure and, following our roadmap, we took decisive steps to strengthen our financial structure. Although the results are still far from our potential, we are confident that the efforts undertaken over the past two years have laid a solid foundation for the next stages of Kering's development," comments François-Henri Pinault, Chairman and CEO of the French group.

Operating free cash flow in the first half year amounted to EUR 2.4 billion, of which EUR 1.3 billion came from real estate disposals.

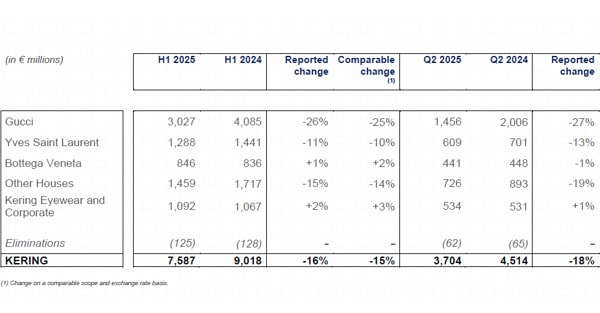

The performance of individual brands

.A heavy half-year for Gucci. The group's main fashion house posted revenues of €3 billion, down 26% (reported), following a 42% slump in the wholesale channel, while the retail network posted -24%. "In the second quarter, sales showed a slight sequential improvement, supported by performance in North America and Asia Pacific. The new leather goods lines, in particular the 'Giglio' bag launched in the Cruise 2026 collection, were a strong success," the statement read. Gucci's recurring operating profit was €486 million, with a margin of 16%, down 8.7 percentage points year-on-year.